Key Takeaways

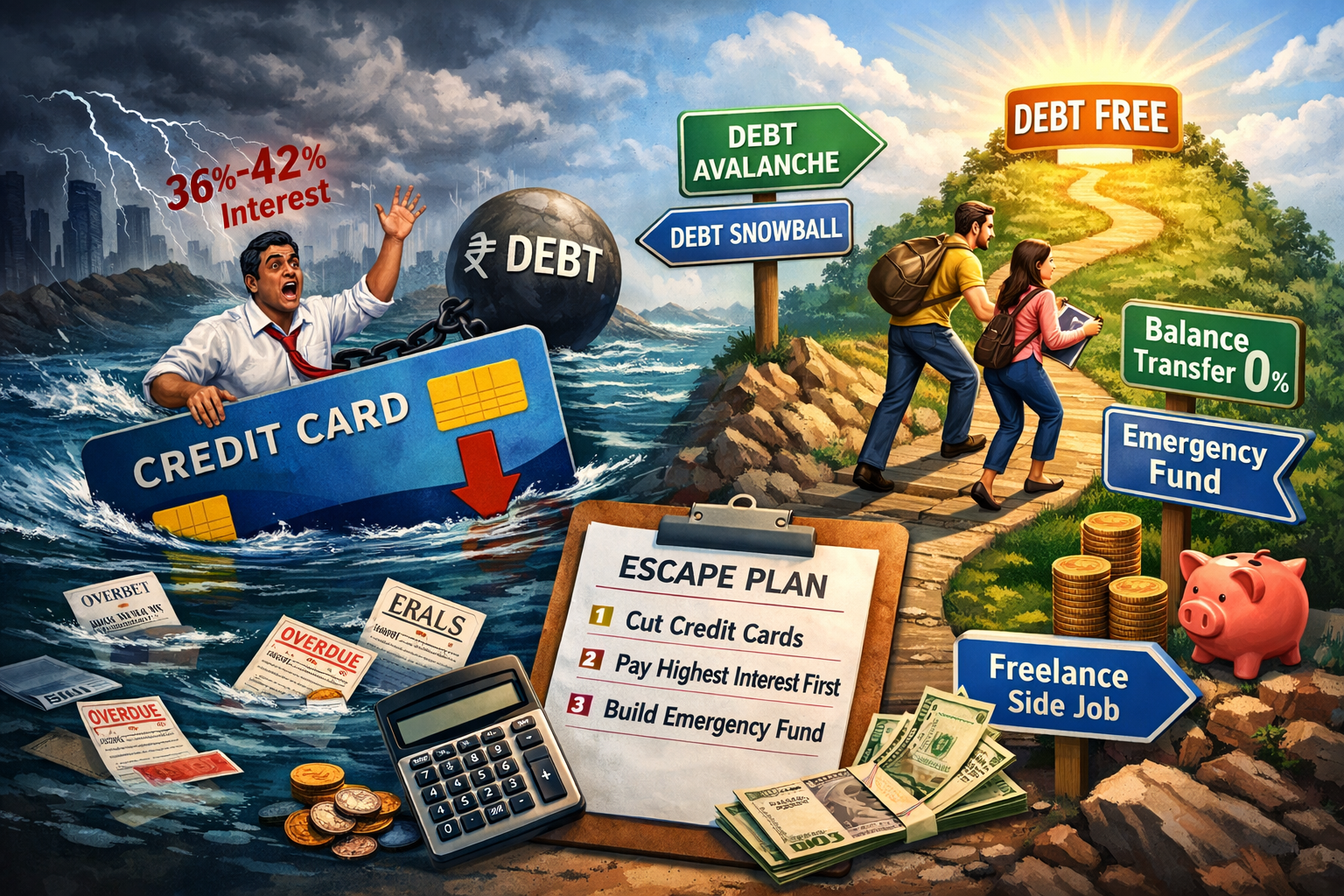

- Credit card debt is toxic at 36-42% annual interest—3-5x higher than personal loans.

- ₹1 lakh minimum payments take 22 years to clear and cost ₹2.84 lakh in interest alone.

- Debt Avalanche method (attack highest interest first) saves the most money mathematically.

- Balance transfer to 0% interest cards buys you time to pay down principal aggressively.

- Prevention is key—build an emergency fund to avoid future credit card reliance.

If you're drowning in credit card debt, you're not alone. Credit card defaults in India are rising as more people fall into the "minimum payment trap." At 36-42% annual interest, credit card debt is one of the most toxic forms of borrowing.

The good news? You can escape this trap with a solid plan, discipline, and the right strategies. This guide shows you exactly how to clear your credit card debt and rebuild your financial life.

Why Credit Card Debt is So Dangerous

Credit cards charge interest rates between 36-42% per year (3-3.5% per month). To put this in perspective:

| Loan Type | Typical Interest Rate | Monthly Interest on ₹1 Lakh |

|---|---|---|

| Home Loan | 8% p.a. | ~₹667 |

| Personal Loan | 12-15% p.a. | ~₹1,000-₹1,250 |

| Credit Card | 36-42% p.a. | ~₹3,000-₹3,500 |

If you owe ₹50,000 and only pay the minimum (5% or ₹2,500), you'll pay interest on the remaining ₹47,500. At 3.5% monthly interest, that's ₹1,662 in interest alone. Your payment barely touches the principal.

The Minimum Payment Trap

Example: You owe ₹1,00,000 on your credit card. If you only pay the 5% minimum (₹5,000/month), it will take you 265 months (22 years!) to pay it off, and you'll pay ₹2,84,968 in interest.

Total paid: ₹3,84,968 for a ₹1 lakh expense!

This is why minimum payments are designed to keep you in debt forever. Banks profit from your struggle.

Step 1: Stop the Bleeding — No New Debt

First rule: Stop using the card. You can't bail water out of a sinking boat if you keep making new holes.

Immediate Actions:

- Physically cut up your credit card or freeze it in a block of ice

- Remove it from online wallets (Amazon, Swiggy, Zomato, etc.)

- Switch to debit card or UPI for all purchases

- Track every expense to eliminate waste

- Delete shopping apps from your phone temporarily

This step is psychological warfare. If the card isn't accessible, you can't use it impulsively.

Step 2: List All Your Debts

You can't fight an enemy you can't see. Make a complete debt inventory:

Information to Gather:

- Card Name (e.g., HDFC Regalia, SBI SimplyCLICK)

- Outstanding Balance

- Interest Rate (find this in your statement or call customer care)

- Minimum Payment Due

- Due Date

Example Debt List:

- HDFC Regalia: ₹80,000 @ 42% p.a. (Minimum: ₹4,000)

- ICICI Platinum: ₹40,000 @ 38% p.a. (Minimum: ₹2,000)

- Axis Neo: ₹25,000 @ 40% p.a. (Minimum: ₹1,250)

Total Debt: ₹1,45,000

Looking at this number might be scary, but you MUST face it. Ignorance won't make the debt disappear.

Step 3: Choose a Payoff Strategy

There are two proven methods. Both work—pick the one that matches your personality.

Strategy A: Debt Avalanche (Mathematically Optimal)

Pay minimums on all cards, then throw every extra rupee at the card with the highest interest rate.

Using our example:

- Attack HDFC (42%) first → Save maximum interest

- Then Axis (40%)

- Finally ICICI (38%)

Why it works: You eliminate the most expensive debt first, saving you hundreds (or thousands) in interest charges.

Strategy B: Debt Snowball (Psychologically Motivating)

Pay minimums on all cards, then attack the card with the smallest balance first.

Using our example:

- Clear Axis (₹25,000) first → Quick win!

- Then ICICI (₹40,000)

- Finally HDFC (₹80,000)

Why it works: Small wins keep you motivated. Seeing one card go to ZERO balance gives psychological momentum to tackle the next.

Which should you choose? If you're disciplined, choose Avalanche (saves more money). If you need motivation, choose Snowball (easier to stick with).

Step 4: Free Up Cash to Attack Debt

Paying minimums won't cut it. You need to find extra money to throw at this debt. This requires temporary sacrifice.

Income Optimization:

- Take up a side hustle: Freelancing, tutoring, weekend gigs (₹5,000-₹15,000/month)

- Sell unused items: Old phone, unused gadgets, clothes on OLX/FB Marketplace

- Use windfalls 100%: Bonuses, tax refunds, gifts → straight to debt

- Negotiate a raise: If you're performing well, ask for one

Expense Elimination (Temporary):

- Cut all subscriptions: Netflix, Spotify, gym (work out at home)

- No eating out: Cook at home—save ₹5,000-₹10,000/month

- No shopping: Freeze non-essential purchases for 6-12 months

- Use public transport: If possible, save on fuel/auto costs

Every ₹1,000 extra payment saves you hundreds in interest. Apply the 50/30/20 budgeting rule aggressively. Create a family budget and stick to it ruthlessly.

Step 5: Consider a Balance Transfer

Many banks offer balance transfer facilities at 0-1% interest for 6-12 months. You move your high-interest debt to a new card with low/zero interest.

How It Works:

- Apply for a balance transfer card (SBI Card, HDFC, ICICI offer these)

- Processing fee: 1-3% of transferred amount (e.g., ₹2,000 on ₹1 lakh transfer)

- Interest-free period: 6-12 months (check terms carefully)

- After period ends, interest jumps back to 36-42%

Strategy:

Use the 0% period to aggressively pay down the principal without interest bleeding you dry. Set a calendar reminder to clear it before the promotional period ends.

Example: Transfer ₹1 lakh at 1% fee (₹1,000). You have 12 months interest-free. Pay ₹8,334/month = clear in 12 months. Total cost: ₹1,01,000 instead of ₹1,84,968 with minimum payments!

Balance Transfer Warning

Do NOT use this as an excuse to avoid paying. Many people transfer balances, feel relief, then run up the old card again. You'll end up with DOUBLE the debt.

Only do balance transfer if you commit to not using ANY credit cards during the payoff period.

Step 6: Personal Loan to Consolidate (Last Resort)

If your debt is massive (₹2 lakh+), consider taking a personal loan at 12-15% to pay off all credit cards.

Pros:

- Lower interest (12-15% vs 36-42%) — Save ₹20,000-₹30,000/year

- Fixed EMI forces discipline

- Clear end date (24-60 months)

- Can't keep adding to the balance (unlike credit cards)

Cons:

- Processing fees and charges (1-3%)

- Affects CIBIL score temporarily (enquiry + utilization)

- Temptation to use cleared cards again (DON'T!)

- Prepayment penalties on some loans

Only do this if:

- You're committed to not running up card balances again

- The interest savings are significant (check total cost)

- You cut up the credit cards immediately after clearing them

Step 7: Negotiate with Your Bank

If you're really struggling, call your bank's customer service. Be honest about your situation and ask for help:

What to Request:

- Interest rate reduction: Sometimes they'll lower from 42% to 24% (still high, but better)

- Waiver of late fees: If you have good payment history, they might waive penalties

- Structured payment plan: EMI to clear dues over 6-12 months

- Settlement option: In extreme cases, they may accept 70-80% of balance as full settlement

Script to use: "I'm committed to paying off this debt, but I'm struggling with the current interest rate. Is there any way we can work out a payment plan or reduced interest so I can clear this faster?"

Banks would rather get their money back slowly than not at all. Be honest, be polite, and ask firmly.

Preventing Future Credit Card Debt

Once you're debt-free, you never want to return to this nightmare. Here's how to stay safe:

1. Build an Emergency Fund

Most credit card debt starts with an emergency (medical bill, job loss, unexpected repair). Build a 6-month emergency fund so you're not forced to swipe cards in crisis.

Target: ₹1 lakh minimum, ₹3-5 lakh ideal (based on monthly expenses)

2. Use Credit Cards Smartly (Or Not At All)

If you decide to use credit cards again (for rewards, cashback), follow these iron-clad rules:

- Pay full balance every month (NEVER pay interest)

- Track spending in real-time using banking apps

- Don't use cards for EMI purchases (hidden interest = debt trap)

- Maintain credit utilization below 30% (e.g., ₹15,000 on ₹50,000 limit)

- Set autopay for full statement balance to avoid forgetting

3. Understand Good vs Bad Debt

Learn the difference between good debt and bad debt. Credit card debt for vacations, gadgets, and lifestyle? BAD. Never again.

4. Track Your Net Worth Monthly

Monitor your net worth every month. If liabilities are growing faster than assets, you're moving backward.

You Can Do This

Clearing credit card debt is hard but not impossible. It requires discipline, sacrifice, and a clear plan. Thousands of Indians have escaped this trap—you can too.

Action Steps for Today:

- Stop using credit cards immediately (cut them up if needed)

- List all debts with interest rates and balances

- Choose Avalanche or Snowball method

- Create an aggressive budget (cut all luxuries temporarily)

- Make your first extra payment this week—even if it's just ₹500

Your future self will thank you. Understanding personal finance basics and avoiding common money mistakes will ensure you never fall into this trap again.

Every journey starts with a single step. Today, take that step. Your debt-free life is waiting.

What to read next:

→ Build Your Emergency Fund — Prevent future

debt

→ Good vs Bad Debt — Understand borrowing wisely

→ Calculate Your Net Worth — Track financial progress