Key Takeaways

- Direct and Regular plans are the same fund—same stocks, same manager, same strategy.

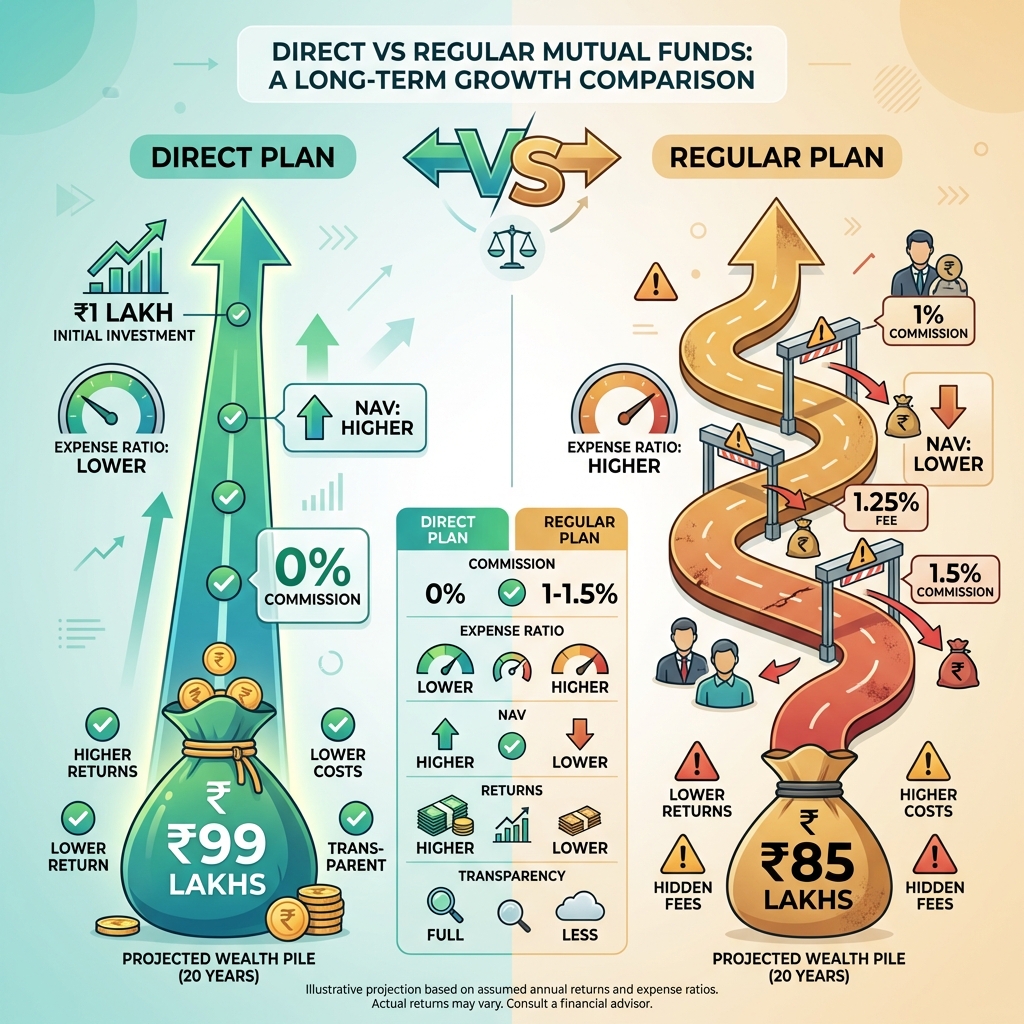

- Regular plans charge 0.5-1.5% extra as commission to distributors (banks, agents).

- A 1% difference = ₹11 lakh lost on a ₹10,000/month SIP over 20 years.

- Direct plans have higher NAV because they don't pay distributor commissions.

- Switching from Regular to Direct may trigger exit loads and capital gains tax—plan carefully.

Imagine you're buying a shirt. You can buy it from a fancy mall showroom for ₹2,000, or you can go to the manufacturer's warehouse and buy the exact same shirt for ₹1,800. The shirt is identical—the fabric, the color, and the brand. The only difference is who you're paying.

This is exactly how mutual funds work in India. Most investors buy "Regular" plans through banks or agents, unknowingly paying a hidden commission every single year. But there's a better way: "Direct" plans.

Let's look at why a seemingly tiny 1% difference in fees can end up costing you the price of a luxury car over your lifetime.

What Are Direct and Regular Plans?

In 2013, SEBI (Securities and Exchange Board of India) mandated that every mutual fund scheme must offer two versions:

Regular Plan:

- Bought through intermediaries — Banks, brokers, financial advisors, insurance agents

- Fund house pays commission to the distributor (0.5-1.5% of your investment annually)

- Higher expense ratio — You bear the cost of this commission

- Lower returns — Due to higher costs eating into your profits

Direct Plan:

- Bought directly — From fund house website or zero-commission platforms

- No middleman commission — Fund house doesn't pay distributors

- Lower expense ratio — You save 0.5-1.5% annually

- Higher returns — More money stays invested and compounds

Critical Fact: They're the SAME Fund

Both Direct and Regular versions invest in the exact same portfolio, managed by the same fund manager, with the same investment strategy.

The only difference is the expense ratio. Direct plans don't pay distributor commissions, so they have lower costs and higher NAV (Net Asset Value).

Direct vs Regular: Side-by-Side Comparison

| Feature | Direct Plan | Regular Plan |

|---|---|---|

| Expense Ratio (Equity Funds) | 0.5% - 1.2% | 1.0% - 2.5% |

| Expense Ratio (Debt Funds) | 0.15% - 0.8% | 0.5% - 1.5% |

| Distributor Commission | Zero (no middleman) | 0.5% - 1.5% annually |

| NAV (Price per Unit) | Higher | Lower |

| Long-Term Returns | Higher (lower costs) | Lower (higher costs) |

| Where to Buy | AMC website, Zerodha Coin, Groww, Kuvera, Paytm Money | Banks, financial advisors, brokers, insurance agents |

| Advisory Support | Self-service (choose your own funds) | Distributor may provide advice |

| Portfolio Management | Same fund manager | Same fund manager |

The ₹11 Lakh Mistake: How 1% Compounds Over Time

Many investors think, "It's just 1%, what's the big deal?" This is the most expensive mistake you can make in investing. Here's why:

The Math:

Let's say you start a SIP (Systematic Investment Plan) of ₹10,000 per month for 20 years. Assume the market grows at 12% annually (before expense ratio).

Scenario 1: Regular Plan (2% Expense Ratio)

- Total investment: ₹10,000 × 12 × 20 = ₹24 lakh

- Actual return after expenses: 12% - 2% = 10%

- Final corpus: ₹76 lakh

Scenario 2: Direct Plan (1% Expense Ratio)

- Total investment: ₹10,000 × 12 × 20 = ₹24 lakh

- Actual return after expenses: 12% - 1% = 11%

- Final corpus: ₹87 lakh

Difference: ₹11 lakh

By simply choosing the Direct version of the exact same fund, you save enough money to buy a premium SUV or fund a significant portion of a child's education.

Real Example: HDFC Top 100 Fund

Direct Plan NAV (Feb 2024): ₹823.45

Regular Plan NAV (Feb 2024): ₹730.12

Same fund, same start date, same investment. The Direct plan is worth 12.8% more purely because of lower expense ratio compounding over 10+ years.

What Is Expense Ratio?

Expense Ratio is the annual fee charged by the mutual fund for managing your money. It covers:

- Fund manager salary

- Research and analysis costs

- Administrative expenses

- Marketing and distribution costs (only in Regular plans)

- Custodian fees and legal costs

How it's charged: The expense ratio is deducted daily from the fund's NAV (Net Asset Value). You don't see a separate bill—it's invisibly subtracted from your returns.

Example:

If a fund has a 1.5% expense ratio:

- For every ₹1,00,000 you invest, ₹1,500 is deducted annually

- If the fund grows 12%, your actual return is 12% - 1.5% = 10.5%

Why Direct Plans Have Lower Expense Ratios:

In Regular plans, the fund house pays 0.5-1.5% commission to distributors. This is called Trail Commission—it's paid every year as long as you stay invested.

In Direct plans, there's no distributor, so no commission. The fund house saves this cost and passes it to you through a lower expense ratio.

How to Check If You're in a Regular or Direct Plan

Method 1: Check Your Account Statement

Log in to your mutual fund app or download your consolidated statement from CAMS or KFintech. Look at the full scheme name:

- Direct Plan: "HDFC Top 100 Fund - Direct Plan - Growth"

- Regular Plan: "HDFC Top 100 Fund - Regular Plan - Growth"

Method 2: Check the NAV

Go to the fund house website and compare NAVs:

- Direct Plan NAV will always be higher

- Regular Plan NAV will be lower (due to extra expenses)

Method 3: Check Expense Ratio

Look at the fund's factsheet (available on AMC website or Moneycontrol):

- Direct plans typically have 0.5-1% lower expense ratio

- This difference is the distributor commission

Should You Switch from Regular to Direct?

If you're currently in Regular plans, switching to Direct can save you lakhs. But there are costs to consider:

1. Exit Load

Most equity funds charge 1% exit load if you redeem (sell) within 1 year of investing.

Strategy: If your holding period is less than 1 year, wait until the exit load period expires before switching.

2. Capital Gains Tax

Switching from Regular to Direct counts as "selling" (redemption), triggering capital gains tax:

- Short-Term (held less than 1 year): 15% tax on gains

- Long-Term (held more than 1 year): 10% tax on gains above ₹1 lakh per year (exemption limit)

Example: You invested ₹1 lakh which is now worth ₹1.5 lakh. If you redeem, you pay 10% tax on ₹50,000 gain = ₹5,000 tax.

3. Is It Still Worth It?

Yes, in most cases. Even after paying 1% exit load and 10% capital gains tax, the long-term savings from lower expense ratios far outweigh the one-time costs.

Smart Switching Strategy:

- For holdings less than 1 year old: Wait until exit load period expires, then switch.

- For holdings more than 1 year old: Calculate tax impact. If gains are under ₹1 lakh, switch immediately (tax-free). If above, spread the switch across years to use the ₹1 lakh exemption.

- For new investments: Always choose Direct plans from now on.

How to Buy Direct Mutual Funds

Option 1: AMC Websites (Fund House Direct)

Buy directly from the Asset Management Company (AMC) websites:

- HDFC Mutual Fund

- ICICI Prudential MF

- SBI Mutual Fund

- Axis Mutual Fund

Pros: Truly direct, no middleman

Cons: You need separate accounts for each AMC (managing 5-10 accounts is

tedious)

Option 2: Direct Mutual Fund Platforms (Recommended)

Use platforms that offer Direct plans from all AMCs in one place:

- Zerodha Coin — Zero commission, no account charges

- Groww — User-friendly, good for beginners

- Kuvera — Advanced portfolio tracking

- Paytm Money — Simple interface

- ET Money — Research tools and recommendations

Pros: One account for all AMCs, easy portfolio tracking

Cons: None (as long as they're genuinely offering Direct plans)

Warning: Verify It's Actually "Direct"

Some platforms claim to be "free" but sell Regular plans and earn commission. Always check:

- The scheme name says "Direct Plan"

- The NAV matches the Direct plan NAV on AMC website

- The expense ratio is lower than Regular plan

Common Myths About Direct Plans

Myth 1: "Direct plans offer lower returns"

False. Direct plans offer HIGHER returns because of lower expense ratios. The portfolio and fund manager are identical.

Myth 2: "I need expert advice, so Regular is better"

Partial truth. If you need advice, hire a Fee-Only Financial Planner. They charge a flat fee (₹5,000-₹50,000 depending on complexity) and help you invest in Direct plans. This is far cheaper than paying 1% commission annually forever.

Myth 3: "Banks offer better service with Regular plans"

False. Direct mutual fund platforms (Zerodha, Groww, Kuvera) offer excellent customer service, portfolio tracking, and tax reports—often better than banks.

Myth 4: "Switching is too complicated"

False. Switching is simple:

- Open account on a Direct MF platform (10 minutes)

- Complete KYC (online, instant if already KYC-compliant)

- Redeem existing Regular plans (one click)

- Invest in Direct plans (one click)

Action Steps: Make the Switch Today

Step 1: Audit Your Portfolio

- Check all your mutual fund holdings

- Identify which are Regular plans (look for "Regular Plan" in scheme name)

- Calculate how much you're losing annually (expense ratio difference × investment amount)

Step 2: Open a Direct MF Account

- Choose a platform (Zerodha Coin, Groww, Kuvera, etc.)

- Complete KYC (Aadhaar + PAN + bank details)

- Link your bank account

Step 3: Stop New Investments in Regular Plans

- Pause all SIPs in Regular plans

- Start new SIPs in Direct plans of the same funds

Step 4: Plan the Switch for Existing Investments

- For holdings less than 1 year: Wait for exit load period to end

- For holdings more than 1 year: Redeem strategically to minimize tax (use ₹1 lakh exemption per year)

- Immediately reinvest redeemed amount in Direct version of same fund

Step 5: Educate Yourself

- Learn to pick index funds (lowest expense ratios, 0.1-0.5%)

- Understand asset allocation (equity vs debt)

- Review portfolio annually

The Bottom Line: Direct Is Always Better

The choice between Direct and Regular is simple: Do you want to pay for advice, or do you want to keep the returns for yourself?

Choose Direct Plans If:

- You're comfortable researching and selecting funds

- You want to invest in index funds (simplest strategy, no active selection needed)

- You can use an app without hand-holding

- You want to maximize long-term returns

Consider Fee-Only Advice + Direct Plans If:

- You need help with financial planning

- You want personalized portfolio construction

- You're willing to pay a one-time or annual flat fee for advice

Avoid Regular Plans Unless:

- You genuinely need ongoing advice and are willing to pay 1% annually for it

- You understand you're trading ₹10+ lakh over 20 years for this service

Remember: The difference compounds. A 1% fee might seem small today, but it can cost you lakhs over decades. Switch to Direct plans and keep that money working for you, not your distributor.

What to read next:

→ SIP Investing Guide — Start systematic investing

→ Assets vs Liabilities — Build real wealth

→ Calculate Net Worth — Track your progress