Here's the uncomfortable truth: saving money keeps it safe, but it doesn't make it grow. And in a country where onion prices can double in six months, "safe" money is actually losing value every single day.

If you grew up in a typical Indian household, the financial advice probably sounded something like this: "Beta, bank mein paisa rakho. FD karvao. Safe rehta hai." Save for a wedding. Save for emergencies. Don't waste money on "unnecessary" things.

And look—saving is a great habit. It's the bedrock of personal finance. But here's what nobody told us: saving alone won't make you wealthy. There's a silent enemy eating away at your carefully saved money, and most of our parents either didn't know about it or chose to ignore it.

That enemy? Inflation.

Saving vs. Investing: What's the Actual Difference?

People use these words interchangeably. Your uncle says he's "investing" in Fixed Deposits. Your friend says she's "saving" for retirement by buying mutual funds. Both are technically wrong.

Saving is parking money somewhere safe for short-term needs. Think emergency fund, next year's vacation, or your kid's school fees. You keep it in a savings account or a liquid fund because you need quick access. The keyword? Preservation.

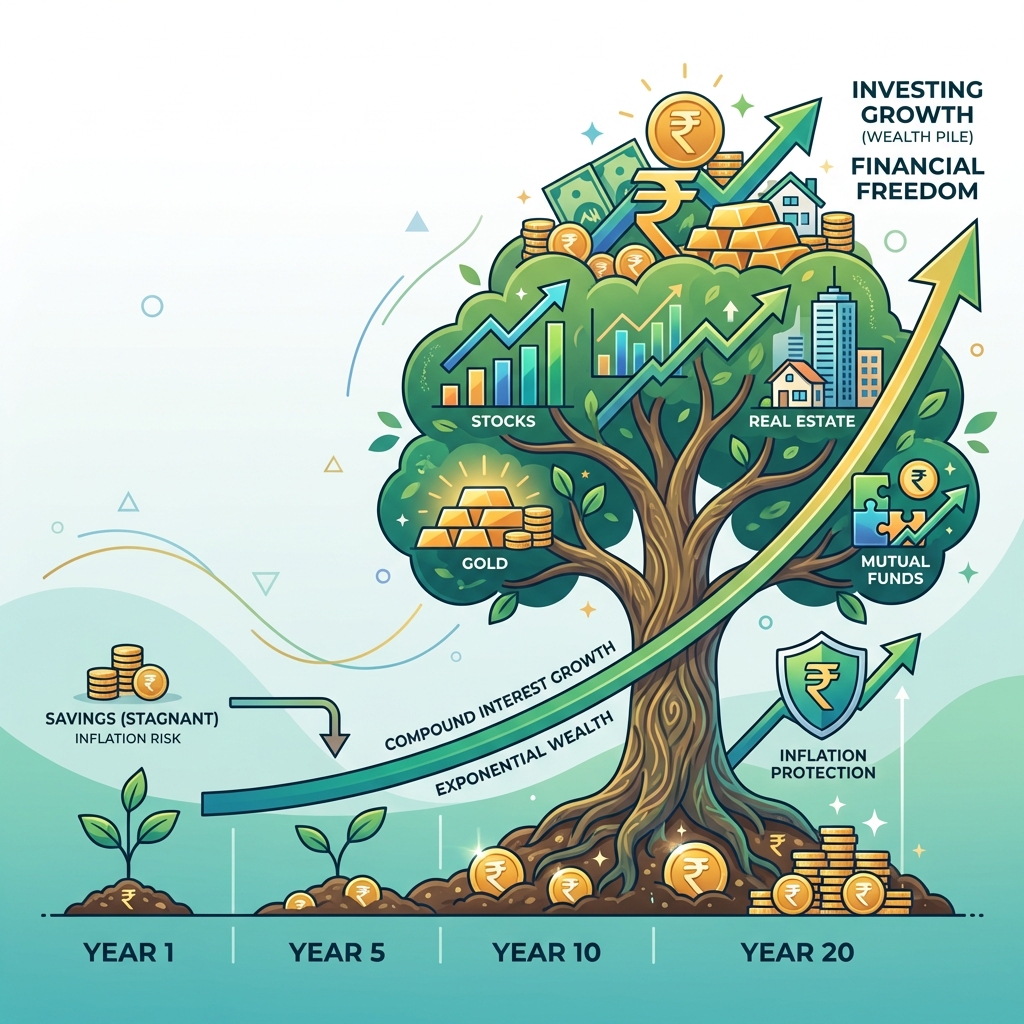

Investing is buying assets that will—hopefully—grow in value over time. Stocks. Mutual funds. Real estate. Even gold (though that's debatable). The keyword? Growth.

The Rule I Wish Someone Told Me at 22:

Saving is for money you'll need in the next

1-3 years.

Investing is for money you won't touch for at least 5-10

years. Longer is better.

Why "Just Saving" Is a Losing Strategy

Let me tell you a story my grandfather loves to repeat. In 1985, he could watch a movie in a theatre for ₹5. Today? That same ticket costs ₹250 (and ₹400 if you want premium seats with recliners).

That's inflation. The silent wealth killer.

In India, prices rise by about 6-7% every year on average. Some years it's higher (remember when petrol hit ₹100+?), some years it's lower. But the trend is clear: everything gets more expensive.

So here's the math: if you stuff ₹100 under your mattress, it's still ₹100 next year. But if inflation is 7%, that ₹100 now has the purchasing power of only ₹93. You didn't lose the note—you lost the value.

"But I keep my money in a bank!" Great. Your savings account gives you maybe 3-4% interest. After inflation eats 6-7%, you're still losing 2-3% every year. Slowly. Quietly. Painfully.

This is why investing isn't a luxury or a choice. It's a necessity. To actually build wealth—not just preserve it—your money needs to grow faster than inflation. If inflation is running at 6%, you need returns of at least 9-10% to make real gains. Savings accounts can't do that. But investments can.

The Magic (Yes, Actually Magic) of Compounding

Einstein allegedly called compound interest the "eighth wonder of the world." He said, "Those who understand it, earn it. Those who don't, pay it."

And honestly? He wasn't exaggerating. Compounding is the closest thing we have to a money-printing machine—if you give it enough time.

Here's how it works. Let's say you invest ₹1 lakh at 10% annual returns (realistic for equity over the long term). After Year 1, you have ₹1.10 lakh. Simple enough.

But in Year 2, you don't just earn 10% on your original ₹1 lakh. You earn 10% on ₹1.10 lakh—including the ₹10,000 profit from Year 1. So you make ₹11,000, not ₹10,000. Your total? ₹1.21 lakh.

Fast forward to Year 20. That single ₹1 lakh deposit—assuming you never add another rupee—grows to over ₹6.7 lakhs. Your ₹1 lakh earned ₹5.7 lakhs just by sitting there and compounding.

Now imagine if you added ₹10,000 every month through a SIP. After 20 years? You'd have close to ₹76 lakhs. The numbers get absurd the longer you invest.

The secret ingredient? Time. Compounding needs years—decades, even—to show its true power. Which is why the best time to start investing was 10 years ago. The second-best time is today.

Where Can You Actually Invest in India?

Alright, so you're sold on investing. Great. Now comes the big question: where do you put your money?

In finance-speak, these options are called "asset classes." Here are the main ones available to Indian investors, ranked roughly from safest (and lowest returns) to riskiest (and highest potential returns).

1. Fixed Income (FDs, PPF, Bonds)

The classic Indian favorite. You're essentially lending money to a bank or the government, and they promise to pay you back with a fixed interest rate. Fixed Deposits, Recurring Deposits, PPF, and government bonds all fall here.

Pros: Very safe. You know exactly how much you'll get.

Cons: Returns are low—usually 6-7%. Barely beats inflation, sometimes

doesn't.

2. Gold

India's emotional hedge. We buy it for weddings, festivals, and "just in case." Gold does act as a decent inflation hedge during uncertain times, but physical gold jewelry has massive making charges (often 15-25% of the price).

Note: Sovereign Gold Bonds (SGBs) were a popular option but have been discontinued by the Indian government. Current alternatives include Gold ETFs (Exchange-Traded Funds), Gold Mutual Funds, or Digital Gold platforms. Each has different cost structures and liquidity features. Learn more in our gold investing guide.

3. Equity (Stocks & Mutual Funds)

This is where real wealth gets built. When you buy equity, you own a tiny piece of a company. If the company grows, your investment grows. Over long periods (10+ years), equity has historically delivered 12-15% returns in India.

You can buy individual stocks (risky, requires research) or invest through mutual funds (diversified, professionally managed). Most beginners should start with mutual funds, specifically index funds.

4. Real Estate

The Indian dream: own a flat, maybe some land. Real estate can be a good investment, but it has problems:

- Requires huge capital (lakhs to crores)

- Very illiquid (can't sell half a bedroom if you need cash)

- High transaction costs (stamp duty, brokerage, maintenance)

For most people starting out, real estate should come after you've built a solid portfolio of liquid investments. Or consider REITs (Real Estate Investment Trusts) if you want real estate exposure without buying property.

Understanding the Risk-Return Relationship

Here's an important principle in investing: if someone promises you "guaranteed 20% returns with zero risk," be extremely skeptical. It's likely either misleading or a Ponzi scheme.

In general, higher potential returns are associated with higher risk and volatility. This isn't a hard rule with zero exceptions, but it's a fundamental principle of investing that's held true historically.

To illustrate this relationship:

- Fixed Deposits: Very predictable. You'll typically get 6-7% returns with minimal risk of losing your principal (plus DICGC insurance up to ₹5 lakh).

- Equity (Stocks/Mutual Funds): Much more volatile. Your portfolio value fluctuates daily. But historically, equity has delivered average returns of 12-15% over long periods (10-15+ years) in India.

The goal isn't to eliminate risk entirely—that's neither possible nor necessarily desirable. Instead, understand your risk tolerance and match your investments to your timeline and goals.

For example: If you need money in 2 years for a house down payment, high-volatility investments like equity might not be suitable—you don't have time to recover from a market downturn. But if you're saving for retirement 20 years away, you have more flexibility to ride out market fluctuations.

The key word is diversification. Don't put all your eggs in one basket. Spread your investments across different asset classes. That's how you balance risk and reward. Learn more in our diversification guide.

How to Start Investing in India

One of the most common misconceptions is that you need large amounts of capital to start investing. Thanks to SIPs (Systematic Investment Plans), you can begin with as little as ₹500 per month.

Here's a general process many people follow:

- Complete KYC verification. You'll need a PAN card and Aadhaar for KYC (Know Your Customer) verification. This is mandatory for regulated financial investments in India.

- Open a Demat Account (if you plan to invest in stocks or certain mutual funds). Many platforms (Zerodha, Groww, Upstox) and banks offer this service, often at low or no cost.

- Define your investment goals. This is crucial. Your timeline significantly impacts what investments might be appropriate. Retirement in 30 years requires a different approach than saving for a car in 3 years.

- Consider starting with SIPs. Many investors begin with index funds or diversified equity funds. Automating monthly investments can help build discipline.

- Track your progress. Periodically review your net worth and portfolio to understand how your investments are performing.

Important: Financial advisors typically recommend building an emergency fund covering 3-6 months of expenses before investing for long-term goals. This ensures you have liquid cash for unexpected events.

The Question of Timing

"Should I wait for the market to drop before investing?"

"Is this a good time to start?"

"What if there's a crash next month?"

These are some of the most common questions in investing. The honest answer? Nobody can predict short-term market movements with consistent accuracy. Not professional fund managers, not market analysts, not anyone.

Markets are inherently unpredictable in the short term. They go up, they go down, and trying to time them perfectly is extremely difficult—even for professionals.

There's a saying in investing: "Time in the market beats timing the market." Historical data suggests that staying invested over longer periods tends to smooth out volatility and capture market growth.

Investing isn't about getting rich quickly or finding the "next big thing." It's a long-term discipline focused on specific goals:

- Building financial independence gradually over time

- Protecting your purchasing power against inflation

- Leveraging the power of compounding to grow wealth

- Creating financial security for yourself and your family

Remember: This article provides educational information only. Before making investment decisions, consider consulting with a SEBI-registered investment advisor who can provide guidance specific to your financial situation, goals, and risk tolerance.