Key Takeaways

- Definition: It is a "Potluck" where you pool money with millions of others to hire a professional Chef (Fund Manager).

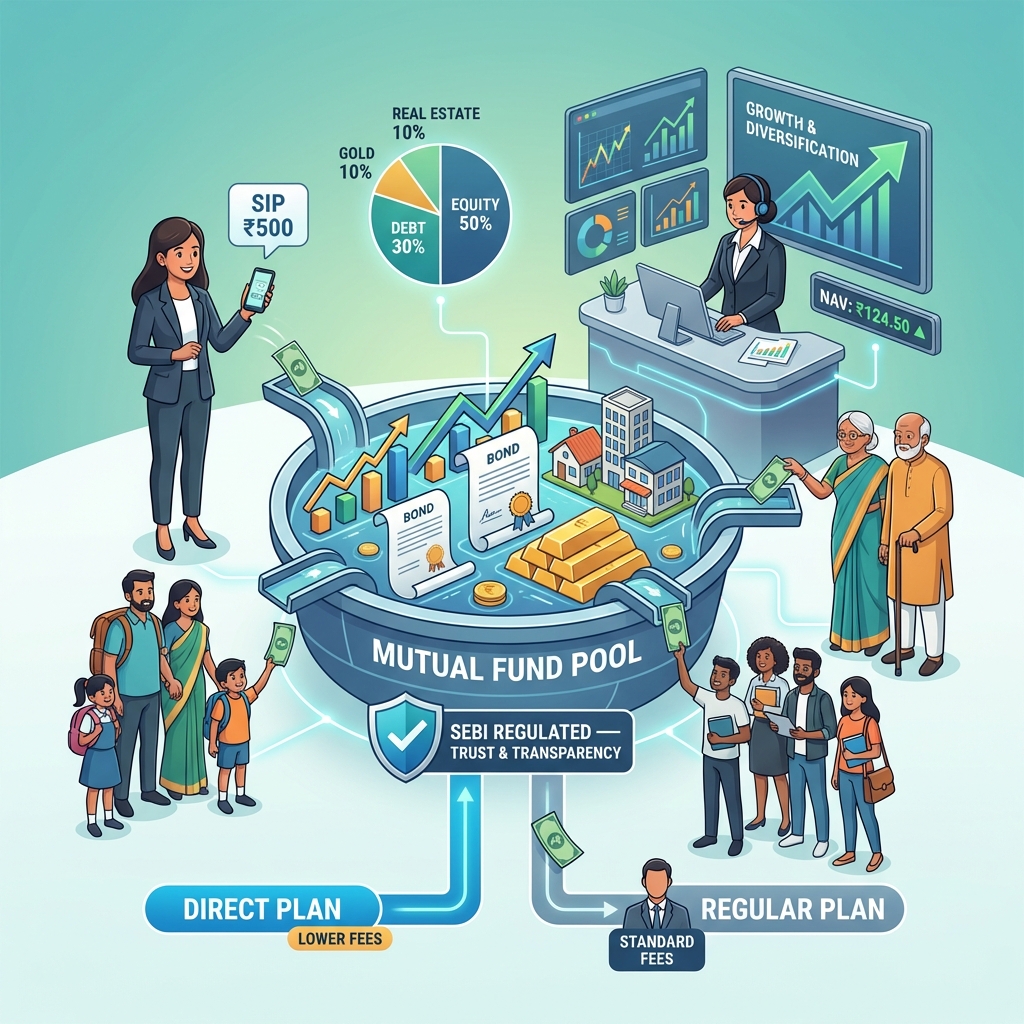

- Safety: Regulated by SEBI. Your money is held by a Custodian, not the Fund Manager.

- Types: Equity (Growth), Debt (Safety), Hybrid (Mix).

- The Choice: Always choose Growth Option over IDCW (Dividend) to save tax.

- The Trap: Always chose Direct Plan over Regular Plan to save 1% commission every year.

"Mutual Funds Sahi Hai" might be the most famous marketing slogan in Indian finance. But what does "Sahi" mean? Does it mean "Safe"? Does it mean "Guaranteed"?

A Mutual Fund is not a lottery ticket. It is a vehicle. Just like a bus takes 50 people to a destination cheaper than 50 separate cars, a Mutual Fund takes thousands of investors to wealth cheaper than individual stock picking.

1. The "Potluck Dinner" Analogy

Imagine you want to eat a lavish dinner with 50 dishes. Cooking it yourself is impossible

(too expensive, too hard).

So, you and 100 friends pool ₹1,000 each. Now you have ₹1 Lakh.

- The Pool: Mutual Fund Scheme.

- The Chef: Fund Manager (Expert who decides what to buy).

- The Menu: Portfolio (Stocks, Bonds, Gold).

- Your Plate: Units (Your share of the food).

If one dish (Stock) turns out bad, it doesn't ruin your dinner because you have 49 other dishes.

2. Types of Mutual Funds (Simplified)

There are over 2,500 schemes in India. We classify them into 3 simple buckets.

A. Equity Funds (High Risk, High Reward)

These invest in shares of companies.

- Large Cap: Top 100 companies (Reliancell, HDFC, TCS). Stable.

- Mid Cap: Next 150 companies. Faster growth, higher risk.

- Small Cap: Smaller companies. Very risky, but can double in value quickly.

B. Debt Funds (Low Risk, Low Reward)

These lend money to the Government or Corporates. They are safer than stocks.

- Liquid Funds: Safe place to park money for 1-3 months. Better than Savings Account.

C. Hybrid Funds (Balanced)

A mix of both. Typically 65% Equity and 35% Debt. Good for beginners.

3. Clearing the Confusions

When you go to buy a fund on an app (like Zerodha/Groww), you see confusing names. Let's decode them.

Direct vs Regular Plan

This is the most important decision you will make.

| Feature | Direct Plan | Regular Plan |

|---|---|---|

| Commission | Zero | 1% to Agent |

| Returns | Higher | Lower (by 1%) |

| Name Contains | "Direct" | "Regular" |

Impact: That 1% difference might look small. But over 20 years on a ₹10,000 SIP, the Regular plan will give you ₹25 Lakhs LESS than the Direct plan. Always choose Direct.

Growth vs IDCW (Dividend)

- Growth: The profit is reinvested into the fund. Your money compounds. Tax is paid only when you withdraw. (Choose This).

- IDCW (Dividend): The fund pays you small amounts periodically. This is bad because your compounding breaks, and you pay tax on every dividend.

4. What is NAV?

NAV = Net Asset Value. It is the "Price" of one unit.

Myth: "A fund with NAV ₹10 is cheaper/better than a fund with NAV ₹500."

Fact: NAV doesn't matter. Only the % growth matters. If both funds grow by

10%, your money grows by 10% regardless of NAV.

5. How Are Returns Taxed? (2026 Rules)

The government takes a share of your profits.

- Short Term (Stubborn): If you sell before 1 year, you pay flat 20% tax on profits.

- Long Term (Patient): If you sell after 1 year, profits up to ₹1.25 Lakhs are tax-free. Above that, you pay 12.5% tax.

(Note: These rates apply to Equity Mutual Funds).

Final Takeaway

Mutual Funds are democratizing wealth. You don't need ₹1 Crore to buy a piece of MRF or Nestle. You just need ₹500 and a Mutual Fund.

Start an SIP in a simple Nifty 50 Index Fund (Direct - Growth). It is boring, simple, and historically effective.