Key Takeaways

- Meaning: SIP (Systematic Investment Plan) is a method to invest small amounts regularly (e.g., ₹500/month).

- The "Good EMI": Unlike a loan EMI that takes money from you, a SIP is an EMI that pays money to your future self.

- No Timing Needed: You don't need to watch the news. SIPs buy more when markets are low (Sale) and less when high.

- Start Small: You can start with just ₹500. The key is consistency, not size.

- Power of 15%: A modest 15% step-up in your SIP every year can double your wealth.

Most Indians think the Share Market is gambling. They are terrified of losing money. SIP is the solution to that fear.

It is the simple, boring, automatic habit that has created more middle-class crorepatis in India than any lottery.

1. What Exactly is SIP?

SIP is NOT an investment product. You cannot "Buy a SIP".

SIP is a method of investing. Just like "Walking" is a method of travel.

- Lumpsum: Investing ₹1 Lakh in one go. (Like jumping to the destination).

- SIP: Investing ₹5,000 every month for 20 months. (Like walking steadily).

The "Good EMI" Analogy

We happily pay EMIs for cars and phones that lose value.

Think of SIP as an EMI for your Freedom. You pay it to your future

self. Once you set it up, it deducts automatically. You learn to live with the remaining

salary.

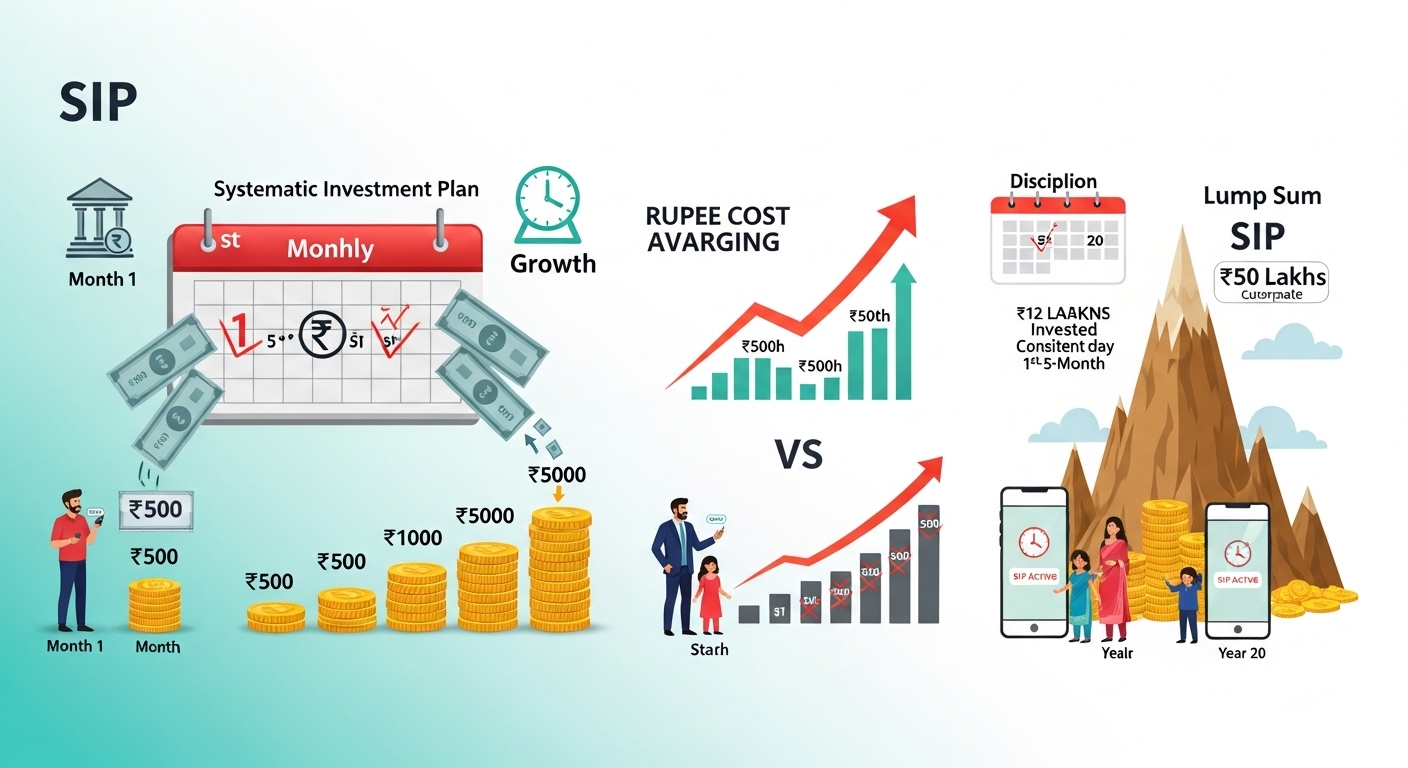

2. Rupee Cost Averaging (The Magic Trick)

Why is SIP safer than Lumpsum? Because of a simple math trick called Rupee Cost Averaging.

Let's say you invest ₹1000 every month in a Mutual Fund.

| Month | Market Status | Price Per Unit (NAV) | Units You Bought |

|---|---|---|---|

| Month 1 | Normal | ₹50 | 20 Units |

| Month 2 | Crashed (Sale!) | ₹25 | 40 Units (Wow!) |

| Month 3 | Booming (Expensive) | ₹100 | 10 Units |

The Result: When the market crashed in Month 2, you automatically bought

MORE units. When it became expensive, you bought fewer.

You don't need to time the market. The SIP does it for you.

3. The ₹10,000 Magic

What happens if you invest ₹10,000 monthly for 20 years?

| Investment Type | Monthly Amount | Total Invested | Final Value (12%) |

|---|---|---|---|

| Recurring Deposit (RD) | ₹10,000 | ₹24 Lakhs | ₹40 Lakhs (approx) |

| Mutual Fund SIP | ₹10,000 | ₹24 Lakhs | ₹1 Crore |

That extra ₹60 Lakhs is the reward for taking a small risk with Equity over limited debt options.

4. How to Kill Your SIP (Mistakes)

Mistake 1: Stopping when the Market falls

This is the biggest wealth destroyer. When the market falls (Red Zone), you get more units

for cheap. That is the BEST time to continue your SIP. If you stop, you lose the benefit of

averaging.

Mistake 2: Not increasing it

Your salary grows every year. Your SIP should too. If you "Step-Up" your SIP by just 10%

every year, your final corpus will be double the normal amount.

5. How to Start?

- KYC: Complete your KYC (One time).

- Pick a Fund: For beginners, a simple Index Fund (Nifty 50) is safest.

- Automate: Set the date to 2 days after your salary day. (e.g., 3rd of every month).

- Forget: Delete the app. Don't look at it daily. Look at it after 5 years.

Final Takeaway

SIP is boring. It is not exciting like trading. But boring makes money.

Start a ₹500 SIP today. Your future self will thank you.